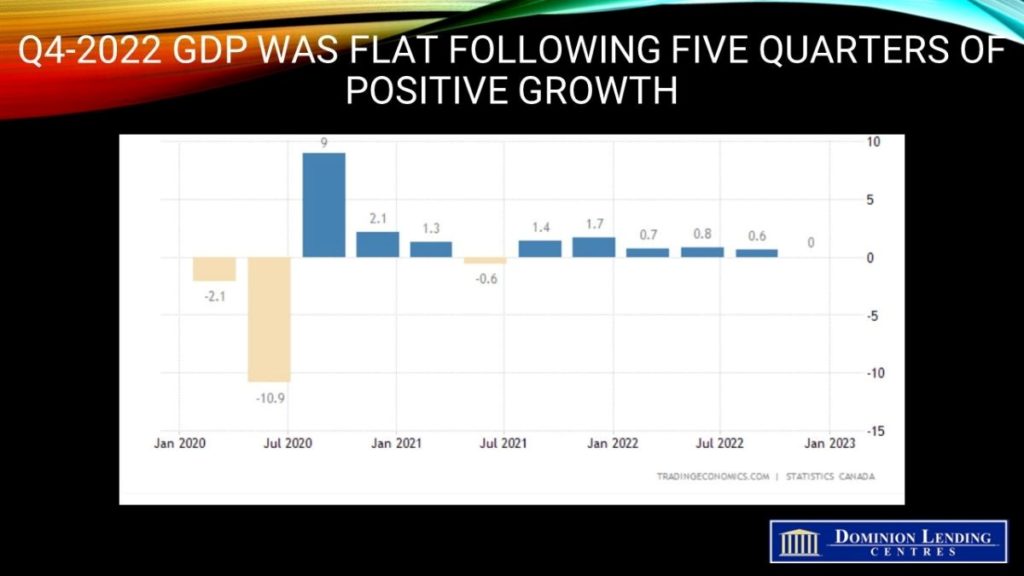

Statistics Canada released the real gross domestic product (GDP) figure for the final quarter of 2022 this morning, showing a marked slowdown in economic activity. This will undoubtedly keep the central bank on the sidelines when they announce their decision on March 8. The Bank had estimated the Q4 growth rate to be 1.3%. Instead, the economy was flat in Q4 at a 0.0% growth rate. This was the slowest quarterly growth pace since the second quarter of 2021.

Inventory accumulation in the fourth quarter declined for manufacturing and retail goods, driving investment in inventories to decline by $29.8 billion. Further, higher interest rates by the Bank of Canada hampered investment in housing (-8.8% at an annual rate), and business investment in machinery and equipment was a weak -5.5%. On the other hand, personal expenditure in the Canadian economy expanded by 2.0% (vs -0.4% in Q3), supported by the red-hot labour market. Government spending growth also accelerated. At the same time, net foreign demand contributed positively to GDP growth as exports grew by 0.8% while imports shrank by 12.0%.

The weak Q4 result reduced the full-year gain in GDP for 2022 to 3.4%, compared to 2.1% in the US, 4.0% in the UK, and 3.6% in the Euro area.

The January GDP flash estimate was +0.3%, pointing towards a rebound in the first quarter of this year. However, flash estimates are always volatile and subject to revision. Nevertheless, the growth in GDP this year will likely be much more moderate, less than 1%.

Bottom Line

The weakness in today’s economic data will be good news to the Bank of Canada, having promised a pause in rate hikes to assess the impact of the cumulative rise in interest rates over the past year. Today’s GDP report and the slowdown in the January CPI inflation numbers portend no interest rate hike on March 8.

Now the Bank will be looking for a softening in the labour market.

Dr. Sherry Cooper | Chief Economist, Dominion Lending Centres

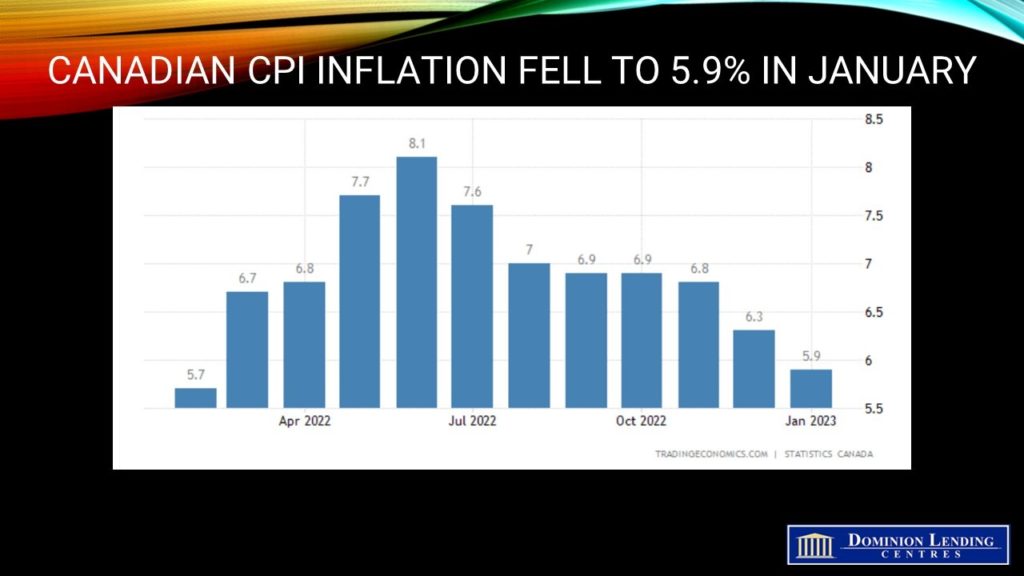

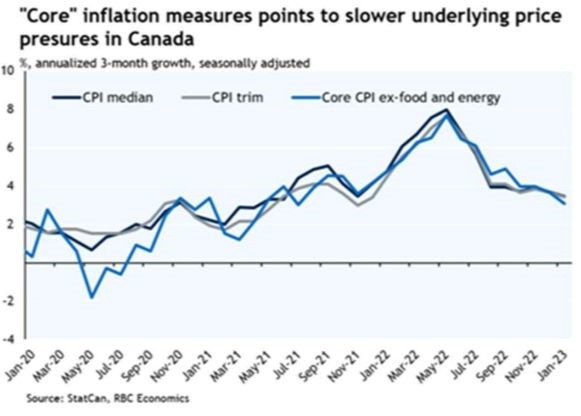

Canadian inflation decelerated meaningfully in January despite the continued strength in the economy. Labour markets remain very tight, and retail sales continue strong. Nevertheless, the Bank of Canada’s jumbo rate hikes over the past eleven months have tempered inflation from a June ’22 peak of 8.1% y/y to 5.9% in January.

Canadian inflation decelerated meaningfully in January despite the continued strength in the economy. Labour markets remain very tight, and retail sales continue strong. Nevertheless, the Bank of Canada’s jumbo rate hikes over the past eleven months have tempered inflation from a June ’22 peak of 8.1% y/y to 5.9% in January. Food prices, however, remain elevated in January (+10.4%) compared to 10.1% in December. Grocery price acceleration in January was partly driven by year-over-year growth in meat prices (+7.3%), resulting from the most significant month-over-month increase since June 2004. Food purchased from restaurants also rose faster, rising 8.2% in January following a 7.7% increase in December.

Food prices, however, remain elevated in January (+10.4%) compared to 10.1% in December. Grocery price acceleration in January was partly driven by year-over-year growth in meat prices (+7.3%), resulting from the most significant month-over-month increase since June 2004. Food purchased from restaurants also rose faster, rising 8.2% in January following a 7.7% increase in December.

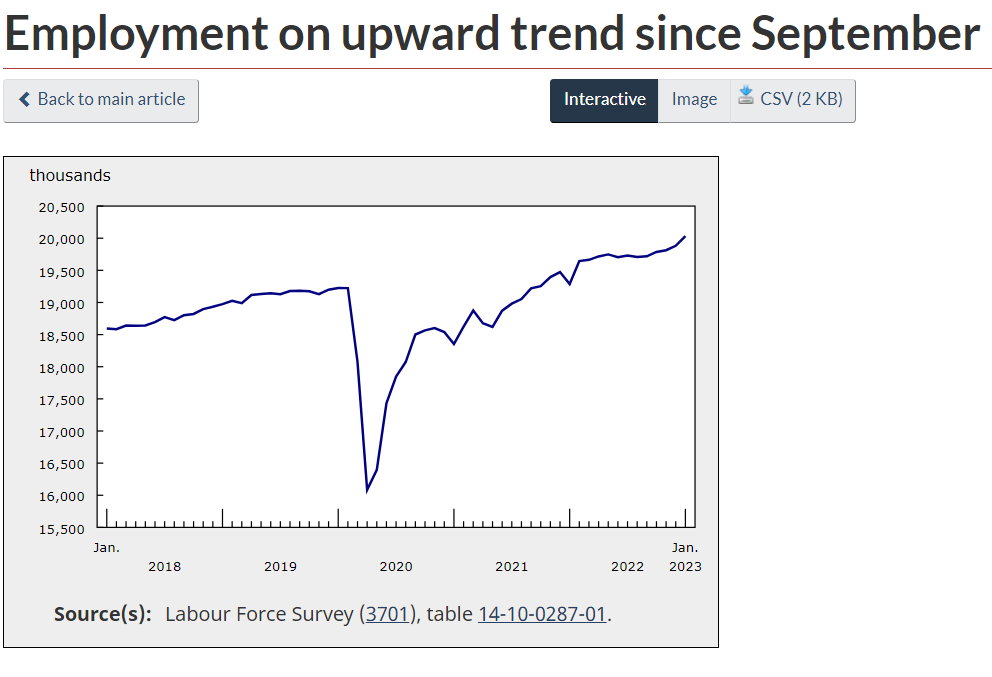

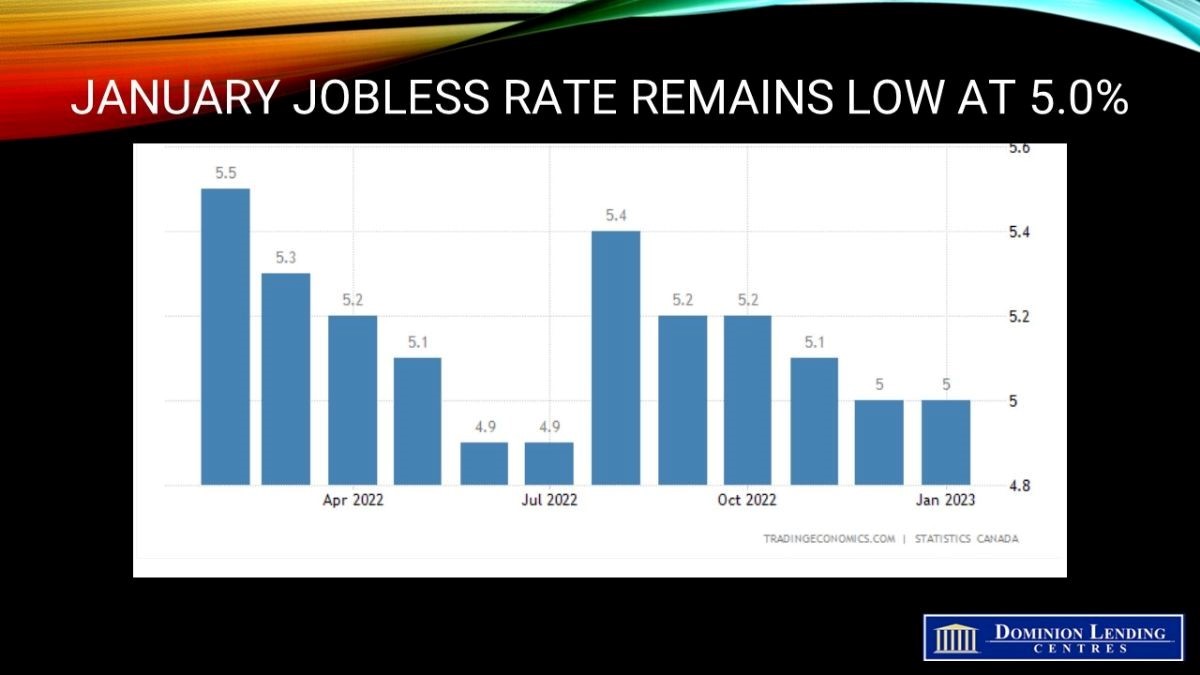

Today’s Labour Force Survey (LFS) for January was much stronger than expected, once again calling into question how long the Bank of Canada’s rate pause will last. This report showed no evidence that the labour market is slowing in response to the vast and rapid runup in interest rates.

Today’s Labour Force Survey (LFS) for January was much stronger than expected, once again calling into question how long the Bank of Canada’s rate pause will last. This report showed no evidence that the labour market is slowing in response to the vast and rapid runup in interest rates.