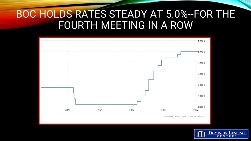

Today, The Bank of Canada held the overnight rate at 5% for the fourth consecutive meeting but provided an outlook suggesting that monetary easing will begin by mid-year. The Bank forecasts a soft landing for the Canadian economy, with inflation falling to 2.5% by the end of this year. While some economists predict a recession, the Bank suggests that “growth will likely remain close to zero through the first quarter of 2024” and “strengthen gradually around the middle of 2024.” This would be a soft landing.

Today, The Bank of Canada held the overnight rate at 5% for the fourth consecutive meeting but provided an outlook suggesting that monetary easing will begin by mid-year. The Bank forecasts a soft landing for the Canadian economy, with inflation falling to 2.5% by the end of this year. While some economists predict a recession, the Bank suggests that “growth will likely remain close to zero through the first quarter of 2024” and “strengthen gradually around the middle of 2024.” This would be a soft landing.

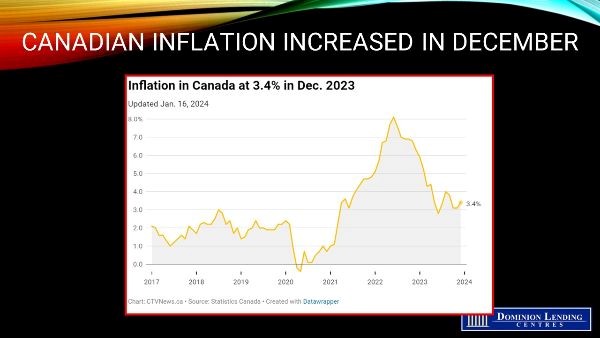

While inflation ended 2023 at 3.4%, owing mainly to high and sticky shelter costs, “the Bank expects inflation to remain close to 3% during the first half of this year before gradually easing, returning to the 2% target in 2025. While the slowdown in demand is reducing price pressures in a broader number of CPI components and corporate pricing behaviour continues to normalize, core measures of inflation are not showing sustained declines.”

The press release says that the “Governing Council wants to see further and sustained easing in core inflation and continues to focus on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour.” The Bank now believes the economy is in excess supply, inflation expectations and corporate pricing behaviour are moving in the right direction, and wage demands, at 5.4% year-over-year in the last reading–are still too high. Wages are a lagging indicator and with job vacancies returning to pre-pandemic levels, wage pressures are likely to dissipate as the year progresses.

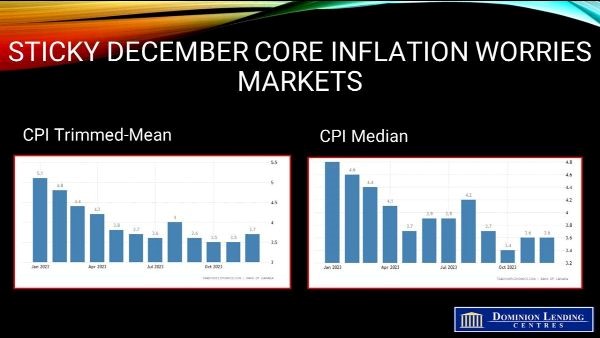

Today, the tone was much more optimistic, suggesting that policymakers are increasingly confident interest rates are restrictive enough to bring inflation back to the 2% target. Still, Bank officials want to see more progress on core inflation before it begins to ease. It said, “The Bank’s preferred measures of core inflation have been around 3½-4%, with the October data coming in towards the lower end of this range.”

The central bank focuses on “the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour” and remains resolute in restoring price stability.

Bottom Line

This was a more upbeat Bank of Canada statement. There is a good chance that monetary tightening has done its job, and inflation will trend downward in the coming months. As we have seen, the road to 2% inflation is bumpy, but we are heading there probably sooner than the Bank expects. As predicted, they are staying the course for now, but multiple rate cuts are likely this year. The scheduled dates for announcing the policy rate are March 6, April 10, June 5 and July 24. The Bank of Canada will begin cutting the overnight rate somewhere in there.

For now, my bet is on the June meeting, but if I’m wrong, it will likely be sooner rather than later. Once they begin to take rates down, they will do so gradually, 25 basis points at a time, and over a series of meetings. We could well see rates fall by 100-to-150 bps this year. Risks to the outlook remain, as always.

I do not expect the overnight policy rate to fall as low as the pre-Covid level of 1.75% this cycle. Inflation averaged less than 2% in the five years before COVID-19, depressed by increasing globalization and technological advances. Those forces are now reversed.