Q3 GDP Weaker Than Expected Paving the Way for Future Rate Cuts

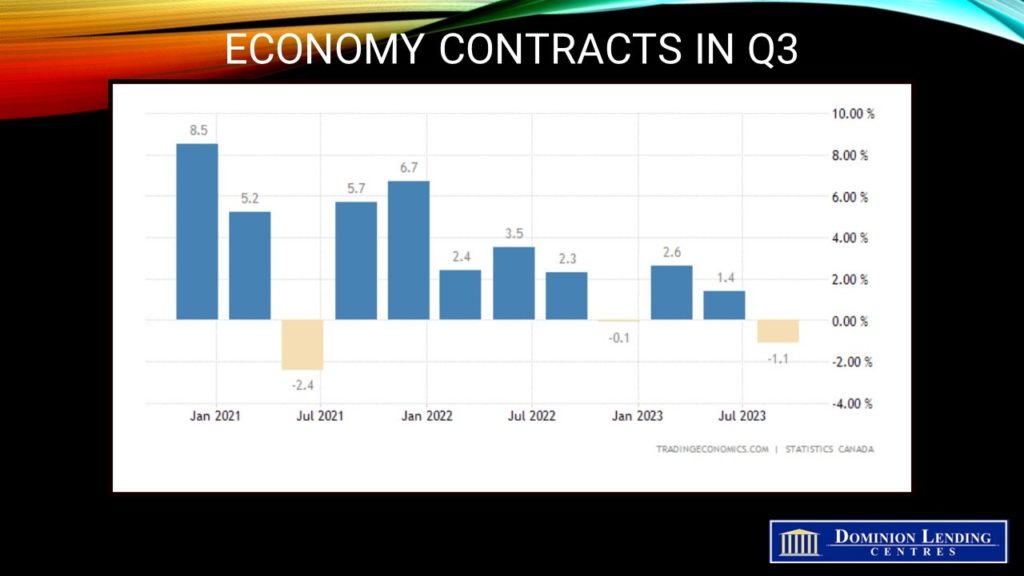

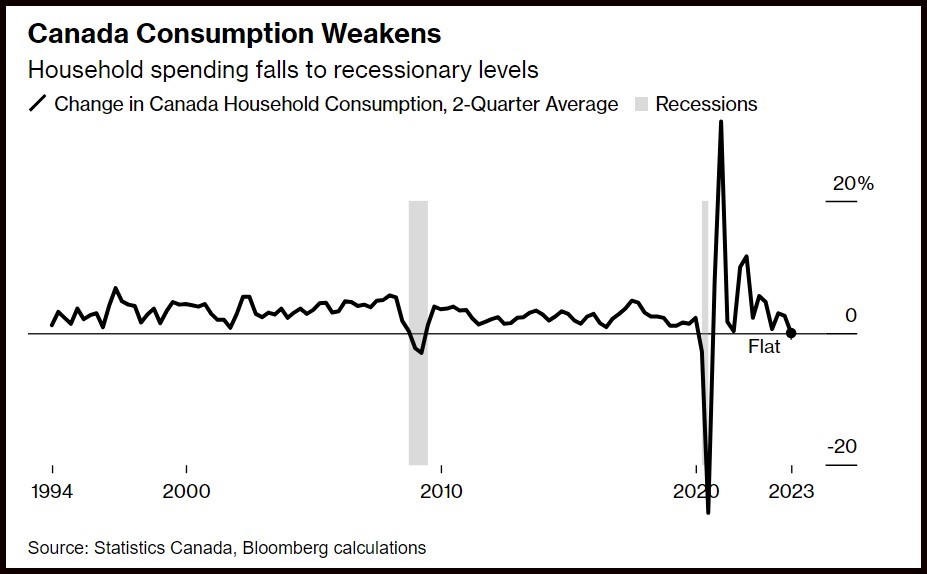

The Canadian economy weakened far more than expected in the third quarter, down 1.1% annually. However, the Q2 figures were revised up significantly from a 0.2% decline to a rise of 1.4%. Such are the vagaries of economic data. The Canadian economy is contracting despite the positive impetus of rapid population growth. Household consumer spending flatlined, and the savings rate rose, confirming that the central bank’s aggressive interest-rate hikes are doing their job to slow economic activity.

The Canadian economy weakened far more than expected in the third quarter, down 1.1% annually. However, the Q2 figures were revised up significantly from a 0.2% decline to a rise of 1.4%. Such are the vagaries of economic data. The Canadian economy is contracting despite the positive impetus of rapid population growth. Household consumer spending flatlined, and the savings rate rose, confirming that the central bank’s aggressive interest-rate hikes are doing their job to slow economic activity.

Statistics Canada also released preliminary data suggesting that GDP grew 0.2% in October, boosted by residential construction and increased oil and gas extraction and retail trade, after the better-than-expected 0.1% expansion in September.

The economic contraction was broadly based. Household spending hasn’t been this weak since 2009, except during the pandemic lockdowns. In addition, business investment was particularly feeble, down 14.4% for business equipment and -7.7% for nonresidential construction. Exports also declined 5.1% over the same period. Investment in residential construction rose 8.3% annualized, the first increase since the beginning of 2022.

Job vacancy data, also released today, posted another decline, confirming that the economy has weakened and excess demand has been eliminated. On a per capita basis, Canada’s economy has contracted for the second consecutive quarter.

Tomorrow, Statistics Canada will release the labour market report for November.

Bottom Line

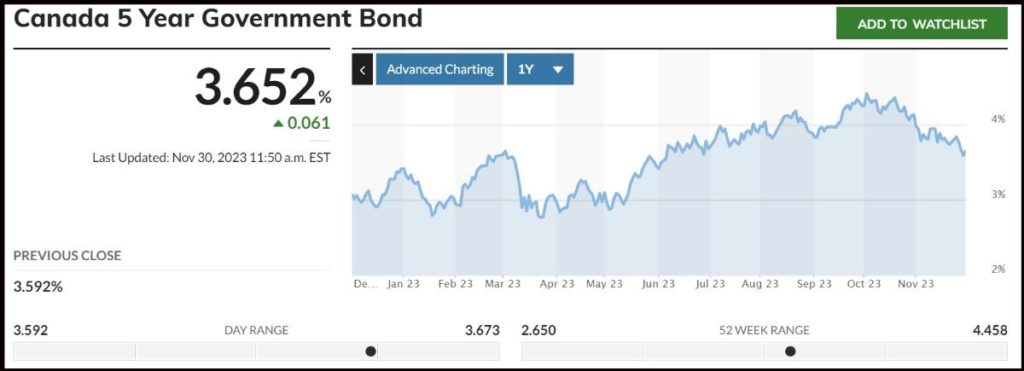

Today’s release is welcome news for the Bank of Canada. Tiff Macklem said last week that the Bank’s interest rate hikes were doing their job to return inflation to its 2% target. The Governing Council meets once again on December 6th. We expect a more dovish press release suggesting that the policy rate has likely peaked. Market-driven interest rates have fallen sharply since early October, taking fixed mortgage rates down significantly (see chart below).

Traders in overnight swaps are betting the Bank of Canada will loosen monetary policy as early as April 2024, little changed from before the release. I expect that the Bank of Canada will gradually cut interest rates beginning in the second quarter of next year, taking the overnight rate down 200 basis points to 3.0% by year’s end.

Building a new home is a super exciting endeavor as you opt to create the perfect space for you and your family. However, building a home is not without its costs and potential surprises… to mitigate bumps on your homebuilding journey and avoid costly mistakes, consider the following tips:

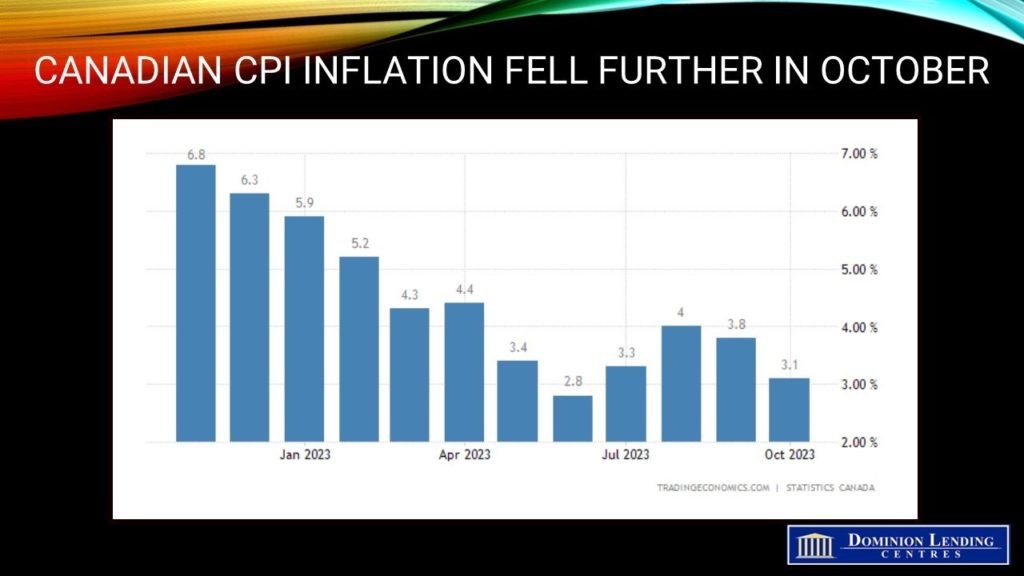

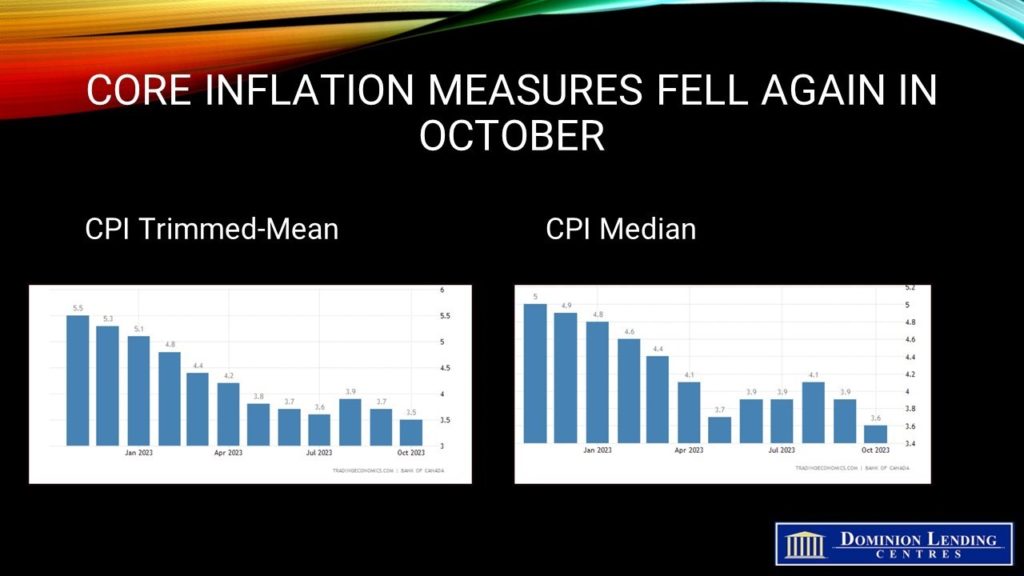

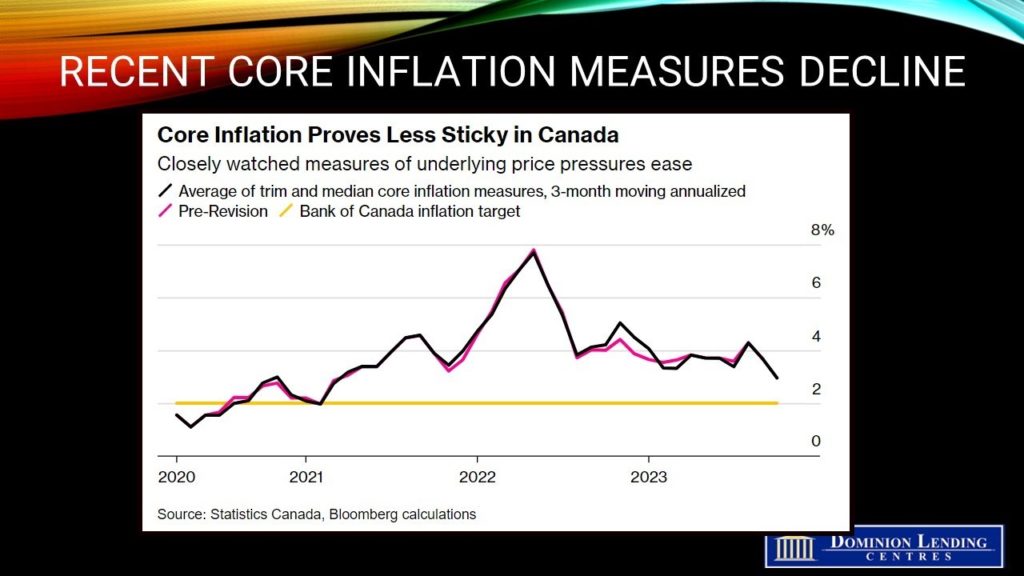

Building a new home is a super exciting endeavor as you opt to create the perfect space for you and your family. However, building a home is not without its costs and potential surprises… to mitigate bumps on your homebuilding journey and avoid costly mistakes, consider the following tips: Today’s inflation report showed a continued improvement, mainly due to falling year-over-year (y/y) gasoline prices. The October Consumer Price Index (CPI) rose 3.1% y/y, down from the 3.8% rise in September. There were no surprises here, so markets moved little on the news. Excluding gasoline, the CPI rose 3.6% in October, compared to 3.7% the month before.

Today’s inflation report showed a continued improvement, mainly due to falling year-over-year (y/y) gasoline prices. The October Consumer Price Index (CPI) rose 3.1% y/y, down from the 3.8% rise in September. There were no surprises here, so markets moved little on the news. Excluding gasoline, the CPI rose 3.6% in October, compared to 3.7% the month before.