Today’s Labour Force Survey for November will do little to assuage the Bank of Canada’s concern about inflation. While employment growth slowed to 10,100 net new jobs–down sharply from October’s reading–the report’s underlying details point to excess labour demand and rising wages. This is compounded by Monday’s data release showing that the Canadian economy grew by 2.9%, double the rate expected by the Bank of Canada. Everyone expects a slowdown in the current quarter and a modest contraction in the new year. However, excess demand is still running rampant in almost everything except housing.

Today’s Labour Force Survey for November will do little to assuage the Bank of Canada’s concern about inflation. While employment growth slowed to 10,100 net new jobs–down sharply from October’s reading–the report’s underlying details point to excess labour demand and rising wages. This is compounded by Monday’s data release showing that the Canadian economy grew by 2.9%, double the rate expected by the Bank of Canada. Everyone expects a slowdown in the current quarter and a modest contraction in the new year. However, excess demand is still running rampant in almost everything except housing.

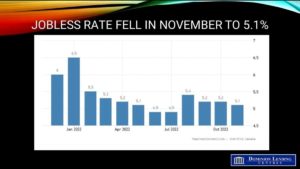

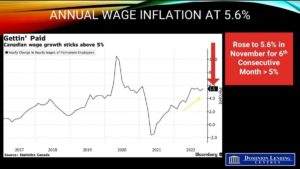

Indicative of hiring strength, full-time employment was up a robust 50,700, and the private sector added 24,700 jobs. The jobless rate ticked down for the second consecutive month to 5.1%–well below the 5.7% rate posted immediately before the pandemic, which was considered full employment at that time. Total hours worked edged up, consistent with growth in the fourth quarter. And most notably, wage inflation came in at a year-over-year pace of 5.6% in November, the sixth consecutive month of greater than 5% wage inflation. Moreover, private and public sector unions demand even more significant wage gains as inflation remains close to 7%.

Businesses report difficulty filling jobs as job vacancies rose in the latest reading. The employment rate among core-aged women reached a new record high of 81.6% in November.

Employment rose in finance, insurance, real estate, rental and leasing, manufacturing, information, culture, and recreation. At the same time, it fell in several industries, including construction and wholesale and retail trade.

While employment increased in Quebec, it declined in five provinces, including Alberta and British Columbia.

Bottom Line

Today’s data are the last key input into the Bank of Canada’s December 7 interest rate decision. Overnight swap markets are fully pricing in a 25 basis-point hike next week, with traders putting about a one-third chance on a 50 basis-point move. Rising wages show no sign of cooling, and the economy posted much more robust growth in the third quarter than the Bank expected.

The overnight policy rate target is currently at 3.75%. If I were on the Bank’s Governing Council, I would vote for a 50-bps rise to 4.25%. Returning to a more typical 25 bps rise is premature, given inflation is a long way above the Bank’s 2% target. Inflation will not slow, with consumers and businesses expecting continued high inflation. Wage-price spiralling is a real risk until inflationary psychology can be broken.

In either case, additional rate hikes early next year are likely. Even when the central bank pauses, it will not pivot to rate cuts for an extended period. Market-driven longer-term interest rates have fallen significantly as market participants expect a recession in 2023. Fixed mortgage rates have fallen as well. The inverted yield curve will remain through much of 2023, with a housing recovery in 2024.