GOOD NEWS on the Inflation Front Suggests Policy Rates Have Peaked

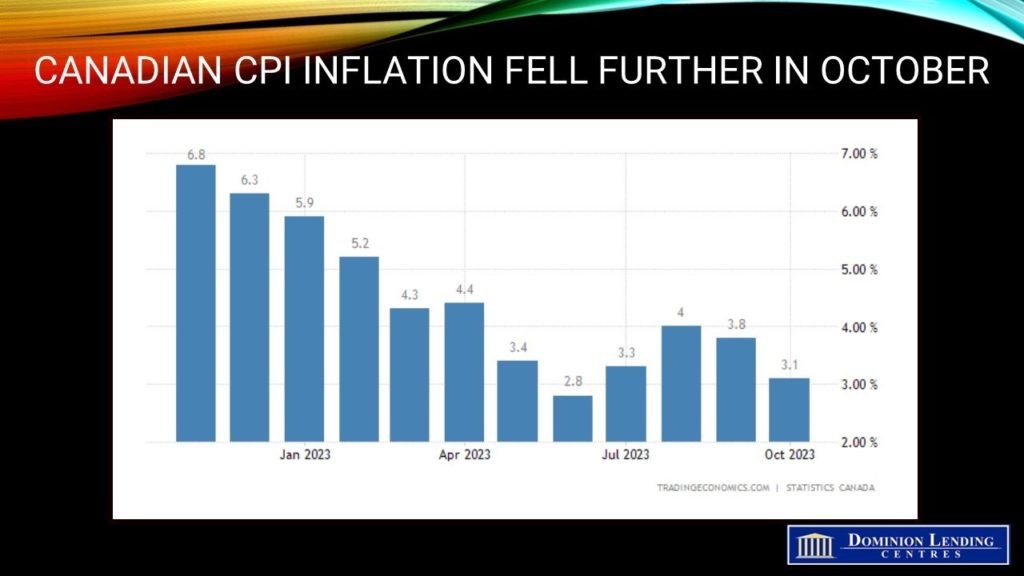

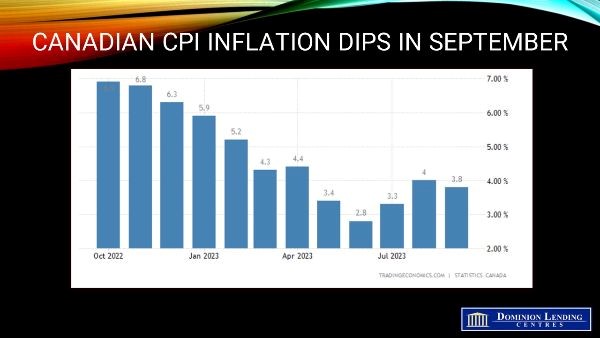

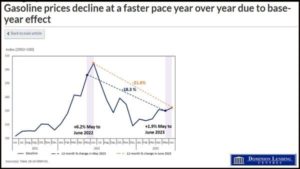

Today’s inflation report showed a continued improvement, mainly due to falling year-over-year (y/y) gasoline prices. The October Consumer Price Index (CPI) rose 3.1% y/y, down from the 3.8% rise in September. There were no surprises here, so markets moved little on the news. Excluding gasoline, the CPI rose 3.6% in October, compared to 3.7% the month before.

Today’s inflation report showed a continued improvement, mainly due to falling year-over-year (y/y) gasoline prices. The October Consumer Price Index (CPI) rose 3.1% y/y, down from the 3.8% rise in September. There were no surprises here, so markets moved little on the news. Excluding gasoline, the CPI rose 3.6% in October, compared to 3.7% the month before.

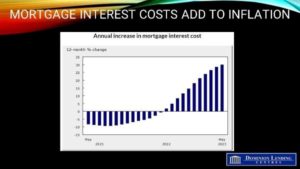

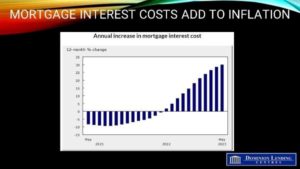

The most significant contributors to inflation remain mortgage interest costs, food purchased at stores, and rent.

Canadians continued to feel the impact of rising rent prices, which grew faster (y/y) in October (+8.2%) than in September (+7.3%). The national increase reflected acceleration across most provinces. The most significant increases in rent prices were seen in Nova Scotia (+14.6%), Alberta (+9.9%), British Columbia (+9.1%) and Quebec (+9.1%).

Property taxes and other special charges, priced annually in October, rose 4.9% yearly, compared with a 3.6% increase in October 2022. The national increase in October 2023 was the largest since October 1992, with homeowners paying more in all but one province, as municipalities required larger budgets to cover rising costs. Property taxes in Manitoba (-0.3%) declined for the third consecutive year, mainly due to reduced provincial education tax.

While goods prices decelerated by -1.6% as prices at the pump fell, prices for services rose 4.6% last month, primarily driven by higher prices for travel tours, rent and property taxes.

While grocery prices remained elevated, they also continued their trend of slower year-over-year growth, with a 5.4% increase in October following a 5.8% gain in September. While deceleration continued to be broad-based, fresh vegetables (+5.0%) contributed the most to the slowdown.

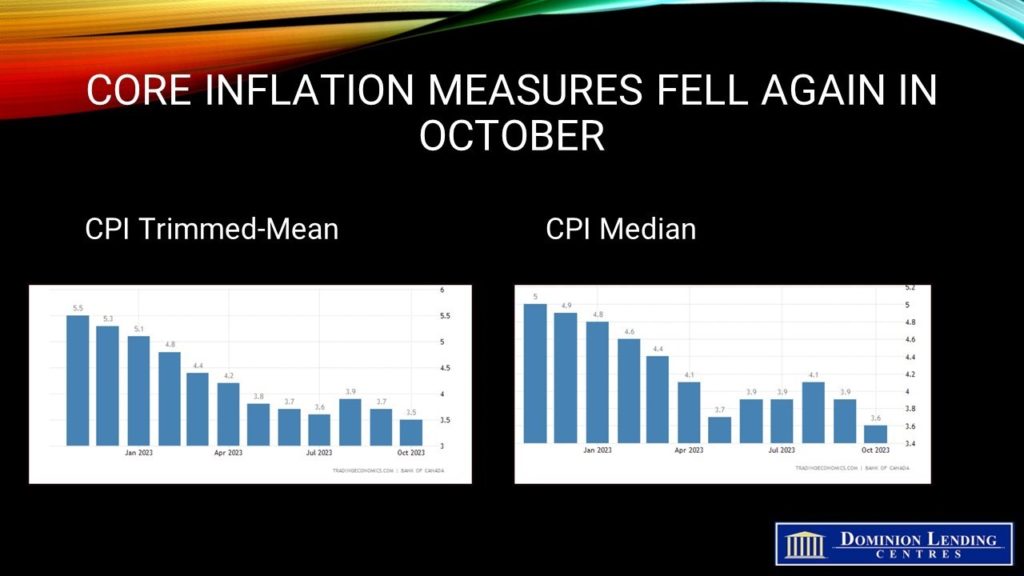

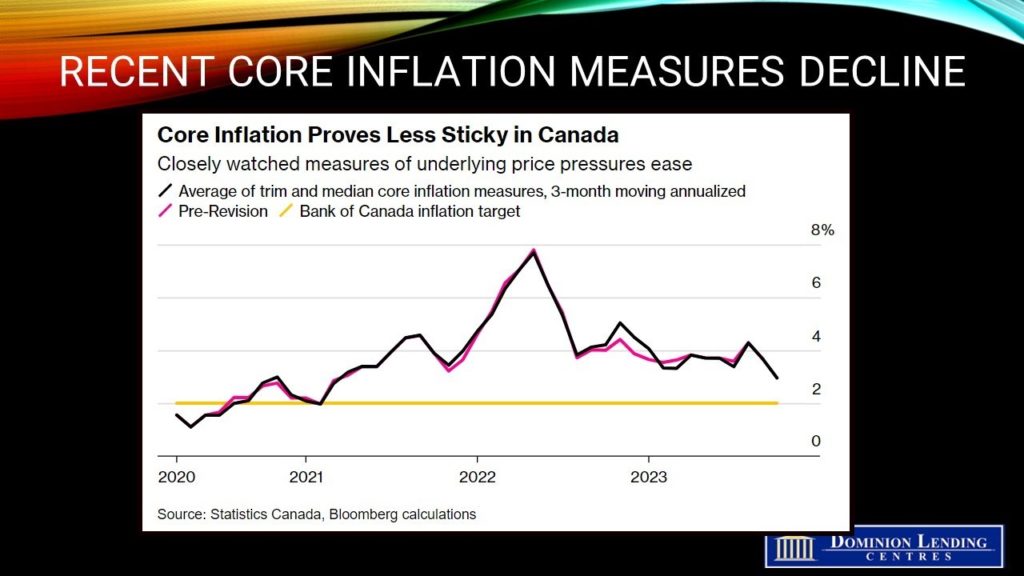

Excluding food and energy, inflation fell to 2.7% in October, down a tick from the September reading. Two other inflation measures closely tracked by the Bank of Canada–the so-called trim and median core rates–also eased, averaging 3.6% from an upwardly revised 3.8% a month earlier.

Bottom Line

According to Bloomberg calculations, another critical measure, a three-month moving average of underlying price pressures, fell to an annualized pace of 2.96% from 3.67% a month earlier. It’s an important metric because Bank of Canada Governor Tiff Macklem has said policymakers are tracking it closely to understand inflation trends.

Today’s news shows that tighter monetary policy is working to bring down the inflation rate. In its Monetary Policy Report last month, the Bank of Canada expected the CPI to average 3.5% through mid-2024. Cutting its economic forecast, the Bank forecasted it would hit its 2% inflation target in the second half of 2025.

Given today’s data and the likely significant slowdown in Q3 GDP growth, released on November 30, and the Labour Force Survey for November the following day, policy rates have peaked. Governor Tiff Macklem will give a speech on the cost of high inflation in New Brunswick tomorrow, and the subsequent decision date for the Governing Council is December 6th. The Bank’s inflation-chopping rhetoric may be relatively hawkish, but the expectation of rate cuts could spur the spring housing market.

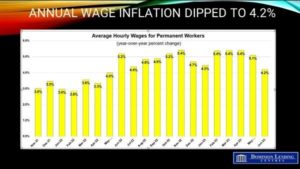

The economists at BMO have pointed out that “three provinces now have an inflation rate below 2%, while only three are above 3%, so much of the country is already seeing serious signs of stabilization. (Unfortunately, the two largest provinces have the fastest inflation rates—Quebec at 4.2% and Ontario at 3.3%).” There is no need for the Bank to raise rates again, and they could begin to cut interest rates in the second quarter of next year.

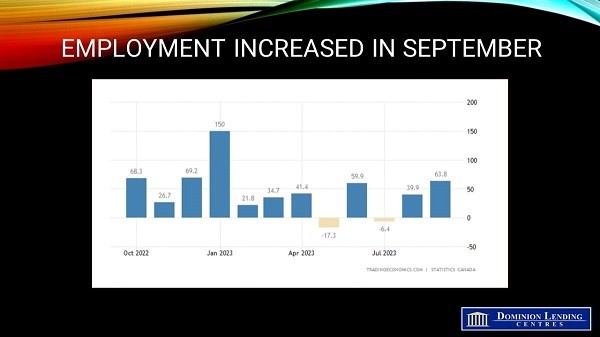

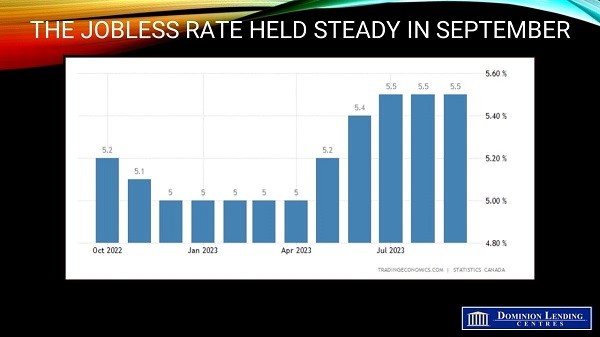

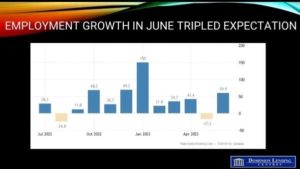

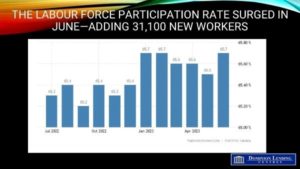

Canadian employment rose by a whopping 63,800 in September, tripling market expectations. The underlying data put the strong job growth into perspective. Most of the gains in overall employment were in part-time work, and total hours worked declined by 0.2%. Moreover, the unemployment rate held steady for the third consecutive month at 5.5% due to a surge in the labour force.

Canadian employment rose by a whopping 63,800 in September, tripling market expectations. The underlying data put the strong job growth into perspective. Most of the gains in overall employment were in part-time work, and total hours worked declined by 0.2%. Moreover, the unemployment rate held steady for the third consecutive month at 5.5% due to a surge in the labour force.

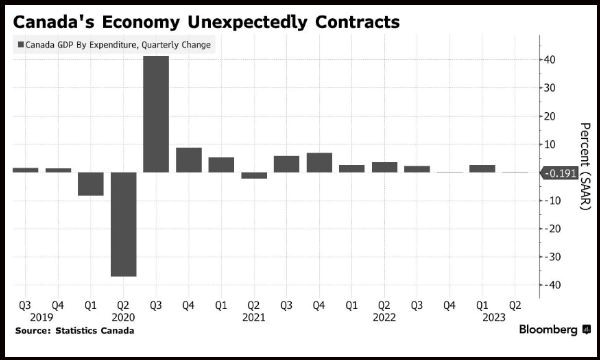

With last Friday’s publication of the anemic second-quarter GDP data, it was obvious that the Bank of Canada would refrain from raising rates at today’s meeting. Economic activity declined by 0.2% in Q2; the first quarter growth estimate decreased from 3.1% to 2.6%.

With last Friday’s publication of the anemic second-quarter GDP data, it was obvious that the Bank of Canada would refrain from raising rates at today’s meeting. Economic activity declined by 0.2% in Q2; the first quarter growth estimate decreased from 3.1% to 2.6%.

The Canadian economy weakened surprisingly more in the second quarter than the market and the Bank of Canada expected. Real GDP edged downward by a 0.2% annual rate in Q2. The consensus was looking for a 1.2% rise. The modest decline followed a downwardly revised 2.6% growth pace in Q1. (Originally, Q1 growth was posted at 3.1%.) According to the latest monthly data, growth dipped by 0.2% in June, and the advance estimate for economic growth in July was essentially unchanged. This implies that the third quarter got off to a weak start.

The Canadian economy weakened surprisingly more in the second quarter than the market and the Bank of Canada expected. Real GDP edged downward by a 0.2% annual rate in Q2. The consensus was looking for a 1.2% rise. The modest decline followed a downwardly revised 2.6% growth pace in Q1. (Originally, Q1 growth was posted at 3.1%.) According to the latest monthly data, growth dipped by 0.2% in June, and the advance estimate for economic growth in July was essentially unchanged. This implies that the third quarter got off to a weak start.

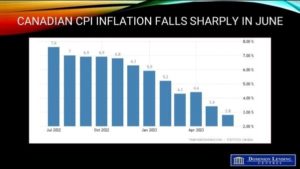

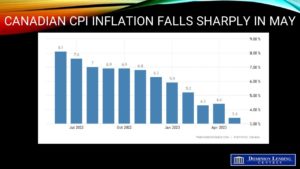

Canadian Inflation Falls Within Bank of Canada’s Target Range; Food and Shelter Costs Remain High

Canadian Inflation Falls Within Bank of Canada’s Target Range; Food and Shelter Costs Remain High The June inflation data provides some relief to consumers, but it is clear that food and shelter costs remain a major concern. The Bank of Canada will closely monitor inflation in the coming months to see if it is on track to return to its 2% target. There is another CPI report before the Bank meets again on September 6th.

The June inflation data provides some relief to consumers, but it is clear that food and shelter costs remain a major concern. The Bank of Canada will closely monitor inflation in the coming months to see if it is on track to return to its 2% target. There is another CPI report before the Bank meets again on September 6th. The Bank of Canada’s underlying inflation measures cooled further in May. CPI-trim eased to 3.7%y/y in June from 3.8% y/y in May, and CPI-median registered 3.9% versus 4.0% y/y in May. The chart below shows the closely watched measure of underlying price pressures, the three-month moving average annualized of the core measures of CPI. They continue to be just under 4%.

The Bank of Canada’s underlying inflation measures cooled further in May. CPI-trim eased to 3.7%y/y in June from 3.8% y/y in May, and CPI-median registered 3.9% versus 4.0% y/y in May. The chart below shows the closely watched measure of underlying price pressures, the three-month moving average annualized of the core measures of CPI. They continue to be just under 4%. Bottom Line

Bottom Line

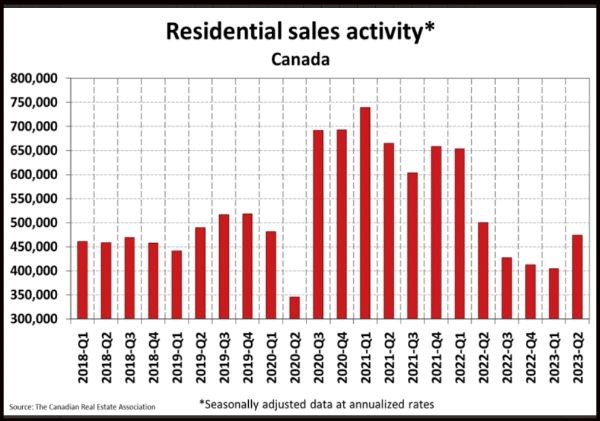

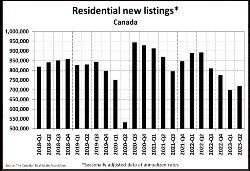

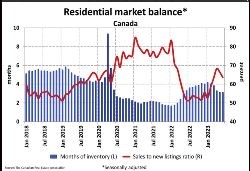

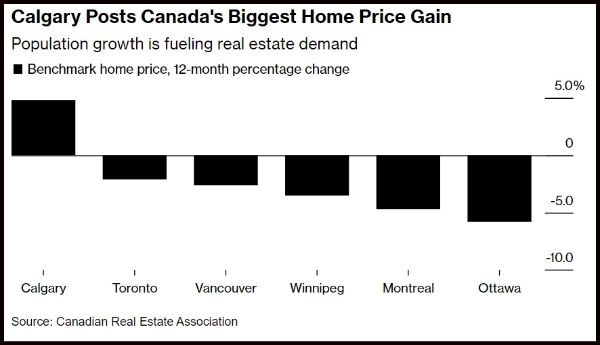

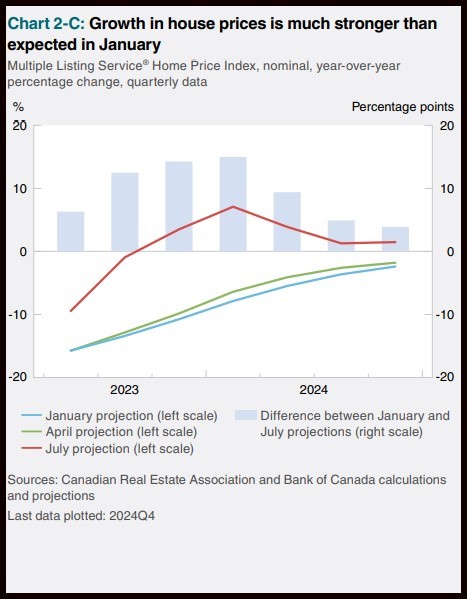

The CREA cut its forecast for home sales this year as tight inventory, and the rate hikes weigh on the housing market. The CREA now estimates that sales in 2023 will be down 6.8% from a year earlier, a more dramatic slowdown than the 1.1% decline forecast in April.

The CREA cut its forecast for home sales this year as tight inventory, and the rate hikes weigh on the housing market. The CREA now estimates that sales in 2023 will be down 6.8% from a year earlier, a more dramatic slowdown than the 1.1% decline forecast in April.

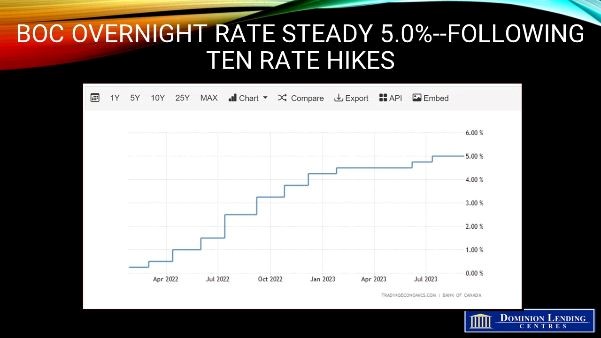

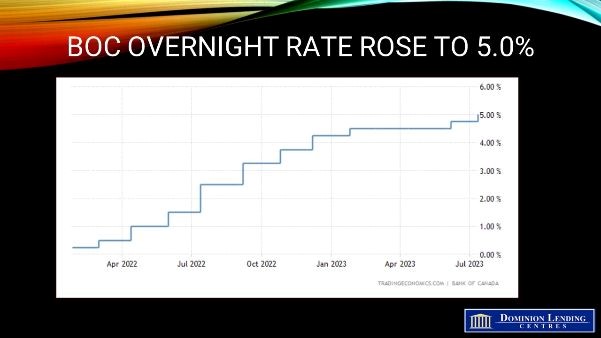

The Bank of Canada increased the overnight policy rate by 25 basis points this morning to 5.0%, its highest level since March 2001. Never before has a policy action been so widely expected. Still, the Bank’s detailed outlook in the July Monetary Policy Report (MPR) suggests stronger growth and a longer trajectory to reach the 2% inflation target. The Bank of Canada believes the economy is still in excess demand and that growth will continue stronger than expected, supported by tight labour markets, the high level of accumulated household savings, and rapid population growth. “Newcomers to Canada are entering the labour force, easing the labour shortage. But at the same time, they add to consumer spending and demand for housing.”

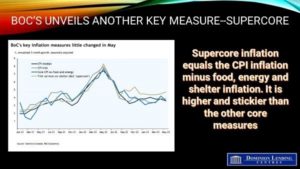

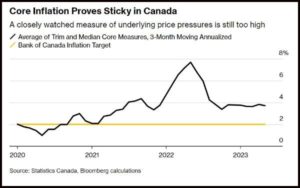

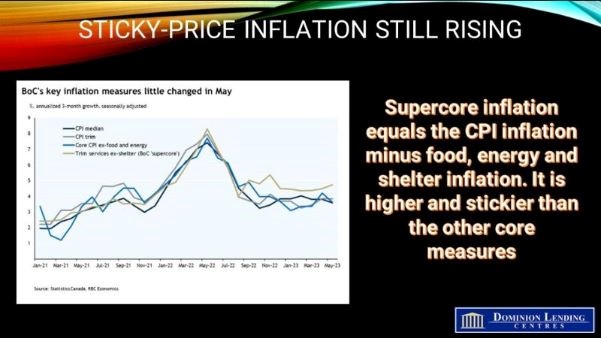

The Bank of Canada increased the overnight policy rate by 25 basis points this morning to 5.0%, its highest level since March 2001. Never before has a policy action been so widely expected. Still, the Bank’s detailed outlook in the July Monetary Policy Report (MPR) suggests stronger growth and a longer trajectory to reach the 2% inflation target. The Bank of Canada believes the economy is still in excess demand and that growth will continue stronger than expected, supported by tight labour markets, the high level of accumulated household savings, and rapid population growth. “Newcomers to Canada are entering the labour force, easing the labour shortage. But at the same time, they add to consumer spending and demand for housing.” There continue to be large price increases in a wide range of goods and services. Measures of core inflation have come down, but by less than expected (see chart below). One measure of core inflation–which removes food, energy and shelter prices, remains elevated and will likely continue to be sticky.

There continue to be large price increases in a wide range of goods and services. Measures of core inflation have come down, but by less than expected (see chart below). One measure of core inflation–which removes food, energy and shelter prices, remains elevated and will likely continue to be sticky. Bottom Line

Bottom Line

The May inflation data, released this morning by Statistics Canada, bore no surprises. The year-over-year (y/y) inflation measured by the Consumer Price Index (CPI) at 3.4% was just as expected–down a full percentage point from the April reading. This is the smallest increase since June 2021. Economists hit this one on the head because we knew dropping the April 2022 figure from the y/y calculation would considerably lower May inflation.

The May inflation data, released this morning by Statistics Canada, bore no surprises. The year-over-year (y/y) inflation measured by the Consumer Price Index (CPI) at 3.4% was just as expected–down a full percentage point from the April reading. This is the smallest increase since June 2021. Economists hit this one on the head because we knew dropping the April 2022 figure from the y/y calculation would considerably lower May inflation.

Prices for durable goods grew at a slower pace year over year in May, rising 1.0% after increasing 2.2% in April. The increase in May is the smallest since May 2020 and coincided with

Prices for durable goods grew at a slower pace year over year in May, rising 1.0% after increasing 2.2% in April. The increase in May is the smallest since May 2020 and coincided with